Navigating the Nuances of Section 1202: Securing a Tax-Free Exit from the Start

When starting a new business, owners are usually not thinking about the day they’ll sell their company. However, imagine building a business from the ground up, dedicating years into its growth, and selling the company without paying any taxes. This sounds too good to be true, but structuring the company to qualify for Qualified Small Business Stock (QSBS) from Day 1 can save owners from paying a hefty tax bill.

Section 1202, which governs QSBS, is essential for small business owners and entrepreneurs looking to structure a new venture. If a company’s stock qualifies as QSBS, the owner(s) can exclude up to 100% of the gain on the sale of the stock from taxable income. Originally enacted in 1993 to incentivize investment in startups, Section 1202 has been a powerful tax-saving tool for founders, early-stage employees, and venture capitalists. The One Big Beautiful Bill Act (OBBBA) expanded the QSBS rules even further, making it easier for small businesses to qualify.

The Core Requirements: Does Your Business Qualify?

To be considered QSBS, the owners and the company must meet several requirements.

Owner Requirements:

1. The Owner must be a non-corporate taxpayer.

The QSBS exclusion applies to non-corporate taxpayers, which generally includes individuals, trusts, and estates. This means that founders, angel investors, employees who receive qualifying stock, and some family members who later receive the stock by gift or inheritance may all potentially benefit from Section 1202, assuming the rest of the requirements are met. A C Corporation, on the other hand, is not eligible to claim the exclusion if it sells the stock of a subsidiary.

Additionally, owners can hold QSBS through a pass-through entity, such as a partnership, an LLC, or an S corporation (for example, a founder's holding company or a venture capital fund). When the pass-through entity sells the QSBS, the tax-free gain flows through to each owner’s individual income tax return.

However, there is one golden rule: you must have been an owner in that pass-through entity on the day it acquired the QSBS, and you must remain an owner at all times until the day the stock is sold.

2. The Owner must acquire the stock directly from the corporation (an “original issuance”).

To qualify as QSBS, the owner generally must acquire the stock directly from the corporation in exchange for cash, property, or services. One key exception is that stock issued in exchange for stock in another corporation is not QSBS.

The original issuance requirement also means that stock purchased from another shareholder is not QSBS. However, stock that qualifies as QSBS can be transferred by gift or upon the owner’s death without losing its QSBS status.

Company Requirements:

1. The Company must be a C Corporation.

The company issuing the stock must be a domestic C corporation when the stock is issued and during substantially all of the owner’s holding period. S corporations, LLCs, and partnerships do not qualify for QSBS benefits. An entity can convert to a state law corporation (or elect to be treated as a C corporation) to take advantage of Section 1202, but additional facts (such as holding periods and built-in gains of the company’s assets) will need to be considered to determine its full effect.

2. The Company must be engaged in an “Active Business.”

The company must use at least 80% of its assets in the active conduct of one or more “qualified trades or businesses.” The tax code defines a qualified business by what it is not. Generally, the code excludes businesses reliant on professional reputation or specific service sectors, including:

Professional services (e.g., law, healthcare, accounting, engineering, consulting)

Financial services (e.g., banking, insurance, leasing, investing)

Farming, mining, or natural resource extraction

Hospitality (e.g., hotels, restaurants)

The General Rule: If your business builds software, manufactures goods, provides non-professional B2B services, or develops physical products, you are likely in the clear. If you provide specialized professional services, you generally will not qualify.

3. The Company cannot exceed a certain amount of Aggregate Gross Assets.

To qualify for QSBS, your company must meet the IRS's definition of a “small business,” which is determined by the company’s aggregate gross assets. There are a few critical nuances that every business owner must understand about this rule:

This is an "At-Issuance" Test: The asset limit is a snapshot taken immediately before and immediately after stock is issued. If the company stays under the limit on the day you receive your shares, your stock will meet the test. If the company later explodes in value and grows to a $500 million valuation, your original stock still qualifies. However, the company will no longer be able to issue new QSBS to future investors or employees.

The Funding Round Trap: Cash from investors counts toward this asset limit. For example, if a scaling company has $45 million in assets and closes a $35 million venture capital round, its assets immediately after the funding round will be $80 million. Because it crossed the threshold, the stock issued to those new investors will fail to qualify as QSBS.

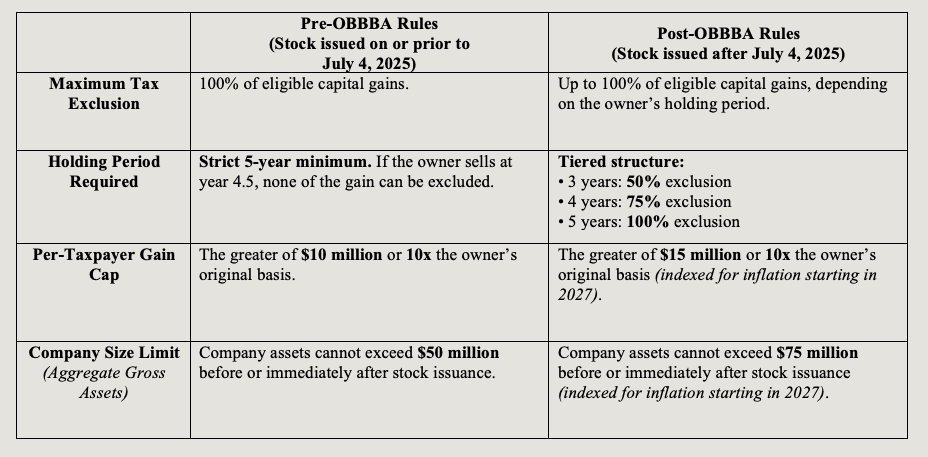

Prior to the OBBBA, the gross asset limitation was a strict $50 million. The OBBBA dramatically expanded this–for stock issued after July 4, 2025, the cap is $75 million (indexed for inflation starting in 2027). This change allows fast-growing startups to raise larger early-stage funding rounds without destroying their QSBS status.

The Big Shift: Pre-OBBBA vs. Post-OBBBA Rules

In addition to raising the aggregate gross asset limitation, the OBBBA made major changes to the QSBS landscape for stock issued after July 4, 2025. If you hold stock issued prior to that date, the old rules still apply. But if you are issuing new equity today, you fall under the expanded, more flexible OBBBA framework.

Here is a side-by-side breakdown of how the laws compare:

Key Takeaways from the New Law:

Faster Liquidity Options: Under the old rules, if an acquisition offer came along at year three or four, founders faced a painful choice: take the money and pay full capital gains taxes, or risk turning down the deal to reach the 5-year finish line. The OBBBA's tiered structure allows for meaningful partial tax exclusions (50% or 75%) on earlier exits.

Larger Companies Allowed: By bumping the asset cap from $50 million to $75 million, the OBBBA allows rapidly scaling mid-market companies to continue issuing tax-free stock to new investors and key hires deeper into their growth cycle.

The Early Exit Lifeline: Section 1045 Rollovers

What happens if an owner sells their business before hitting the new 3-year or historical 5-year marks? The tax code provides an escape hatch under Section 1045.

If you have held your QSBS for at least 6 months but need to sell it, you can defer paying capital gains taxes by rolling over your proceeds into new QSBS (i.e., investing in another qualified company). The rollover must be completed within 60 days of the sale, and the owner’s holding period in the original stock “tacks onto” the new stock, meaning the timeline toward that 100% tax exclusion keeps running.

Common Pitfalls: Where Business Owners Trip Up

Because the tax savings of Section 1202 are so massive, the IRS scrutinizes QSBS claims heavily. A single error during the lifecycle of a company can completely disqualify stock.

Corporate Redemptions: If a corporation buys back its own stock from any shareholder within certain windows before or after issuing new stock, it can inadvertently terminate the QSBS status for all newly issued stock.

Lack of Documentation: You cannot simply cross your fingers and claim a QSBS exclusion on your tax return when you sell your company. Taxpayers must maintain meticulous corporate records proving the company met all of the QSBS requirements throughout the relevant holding period.

State Tax Inconsistency: It is vital to remember that state tax codes do not always mirror federal laws. For example, states like California and Pennsylvania do not recognize the Section 1202 exclusion, meaning owners could still owe state-level capital gains taxes upon the sale.

Weighing the Options: The C Corp Trade-Off

While the promise of a tax-free exit is incredibly compelling, choosing to operate as a C corporation solely to chase QSBS benefits also requires a realistic look at the day-to-day tax trade-offs.

Unlike pass-through entities (like LLCs or S corporations) where business profits flow directly to the owners' personal tax returns, C corporations are subject to double taxation. This introduces two major considerations for your ongoing operations:

The Entity-Level Tax: A C corporation pays a federal corporate income tax on its net profits every year. If you plan to reinvest profits back into scaling the company (common for early-stage tech startups), this corporate tax might not hurt as much. But if the business is highly profitable early on and you want to pull cash out, those profits are taxed first at the corporate level.

Tax on Distributions: When a C corporation distributes its remaining profits to its owners in the form of dividends, those distributions are taxed again on your individual tax return. Distributions from a pass-through entity, on the other hand, are generally not taxed.

For a more in-depth discussion on the taxation of corporations vs. pass-through entities, see our article What should my business be classified as for tax purposes?

The critical question is whether a massive, zero-tax payday at the end of your journey outweighs the burden of paying corporate taxes on profits and dividend taxes on distributions along the way.

For companies aimed at rapid growth, venture capital funding, and an eventual high-value acquisition or IPO, the C corporation structure and the resulting QSBS savings are almost always worth it. For lifestyle businesses or companies intended to distribute steady cash flow to owners year after year, a pass-through structure might still be the smarter play.

The Bottom Line

QSBS is one of the most lucrative corporate tax incentives in existence, and the OBBBA has made it faster to achieve and more accessible to larger businesses. However, capitalizing on these rules requires intentional, proactive legal structuring from Day One.

Whether you are launching a new startup, looking to convert an existing LLC into a C corporation, or planning an upcoming exit strategy, proper legal counsel is essential.

Ready to start? Click here to schedule a consultation with Kalaria Law today to build a proactive tax strategy that protects your hard-earned gains from the beginning.

Disclaimer: This article is for general informational purposes only and does not constitute formal legal advice.