How do I form a legal entity for my business?

Starting a new business is an exciting journey, but before launching a product or service, you need a strong legal foundation. The choice of operating a business as a sole proprietorship or through a separate legal entity, whether a corporation or a limited liability company (LLC), affects everything from your personal liability to how your business is governed and taxed.

This article discusses the key considerations before forming a legal entity for a new business.

1. The Core Decision: To Form a Legal Entity or Not?

Every new business starts somewhere. If you begin selling products or services without filing any formal documentation with the state, your business is automatically classified as a sole proprietorship (if you are the only owner) or a general partnership (if you have co-owners).

The Default Structure: Sole Proprietorship or General Partnership

Sole proprietorships and general partnerships are the most simple forms for operating a business, but they lack the fundamental benefit of separation.

Ease of Formation: No formal state filing is required to start.

Taxation: For sole proprietorships, there is no separate entity for tax purposes. The owner is treated as conducting the business personally, and all income and expenses are reported directly on the owner’s individual income tax return (Schedule C of Form 1040). General partnerships are treated as partnerships for tax purposes and must file an information return (Form 1065, U.S. Return of Partnership Income), even though there is not a separate legal entity.

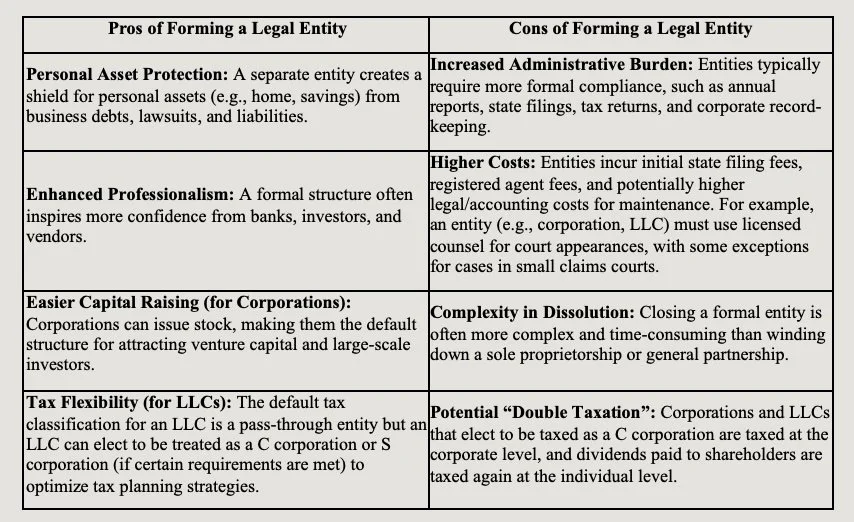

The Major Drawback of Unlimited Personal Liability: Since there is not a separate legal entity, there is no legal distinction between the owners and the business. This means the owners are personally responsible for all business debts, contracts, and legal liabilities. Therefore, the owners’ personal assets—including their homes, savings, and other investments—are at risk if the business faces a lawsuit or cannot pay its debts.

The Decision to Incorporate

Forming a separate legal entity for a business creates a legal barrier between the business and its owners. This vital step grants limited liability and limits the owners’ risk to what they have invested in the entity. Making the choice to form a separate entity is one of the most critical foundational decisions a new owner will make.

2. Choosing Your Structure: Corporation vs. LLC

After making the initial decision to form a separate legal entity for your business, the next question is what type of entity to form. The two primary state-level structures are the corporation and the limited liability company. The choice heavily depends on your operational and long-term financial goals.

The Corporation Structure

A corporation is often favored by public companies and high-growth startups looking to raise venture capital.

Ownership and Governance

Ownership: A corporation is owned by shareholders who receive shares of stock in exchange for their capital investment. Stock issuance is the primary method for raising large amounts of capital from investors.

Authorization and Classes of Stock: The corporation’s Certificate of Incorporation authorizes the total number of shares the corporation is legally allowed to issue. The corporation may also create different classes of stock (e.g., common stock and preferred stock). Preferred stock is typically granted superior rights regarding dividends or liquidation proceeds, making it the standard security offered to venture capital investors.

Shareholders’ Power: Shareholders generally do not manage the day-to-day business of the corporation but are charged with electing the corporation’s Board of Directors.

Governance: The Board of Directors sets the strategic direction and oversees the management of the corporation and appoints the corporation’s officers (e.g., the President and Treasurer). The officers are responsible for the daily operation of the business. This separation of ownership by the shareholders and management by the officers is a defining feature of the corporate structure.

Key Consideration: Maintaining Corporate Status

For a corporation to maintain the crucial benefit of limited liability, shareholders, directors, and officers must strictly adhere to corporate formalities.

Requirements typically include:

Maintaining a corporate charter and bylaws.

Holding regular meetings for the Board of Directors and for the shareholders.

Keeping detailed meeting minutes and corporate records.

Ensuring complete separation of corporate and personal funds.

Failure to do so can lead to a court disregarding the entity’s separate status—a concept known as Piercing the Corporate Veil. If a court “pierces the veil,” shareholders can be held personally liable for the corporation’s debts or wrongdoing.

The Limited Liability Company (LLC) Structure

A limited liability company offers the same personal liability protection as a corporation but with significantly less formality and administrative overhead.

Ownership and Governance

Ownership: An LLC is owned by members who receive membership units or membership interests in exchange for their capital contribution to the LLC. Capital is raised through the sale of these units to new or existing members. The LLC’s governing documents can specify different classes or rights of membership units.

Governance: LLCs offer maximum flexibility in management:

Member-Managed: The members run the day-to-day operations directly. This approach is common for small, owner-operated businesses.

Manager-Managed: The members hire or appoint one or more managers (who may or may not be members) to handle the daily operations. This is often the choice for large LLCs or LLCs with passive investors.

Key Advantages of the LLC Structure:

Flexibility: Fewer mandated formalities (e.g., no mandatory board meetings or minutes required).

Adaptability: LLCs are excellent starting points for most small-to-medium businesses due to their flexibility in ownership and management.

The decision is often a trade-off between the formal structure of a corporation for investor readiness, versus the flexible structure of an LLC for operational simplicity.

3. Jurisdictional Considerations: Delaware vs. Texas

The decision of where to form your entity is crucial. While many businesses choose to incorporate in the state where they physically operate, high-growth companies or those seeking outside investment often choose Delaware.

Professional Entities (PCs and PLLCs)

For businesses providing professional services—such as law, medicine, accounting, or architecture—most states require the use of specialized entities. These entities are designed to accommodate the unique liability structure of professional practice.

Core Principle: Professional entities provide limited liability protection against the business’s debts and the malpractice of other professionals in the firm, but they do not shield the individual professional from liability arising from their own negligence or malpractice.

Available Professional Entities in Delaware and Texas:

Delaware’s statutes primarily recognize the Professional Corporation (PC) for licensed professionals.

Texas offers a more diverse range of specific professional entities (Professional Corporation (PC), Professional Limited Liability Company (PLLC), and Professional Association (PA)), ensuring licensed professionals have clear structures.

4. Understanding Default Federal Tax Classifications

The choice of state law entity will determine the entity’s default classification for federal income tax purposes. An entity’s tax classification determines how the IRS will tax the profits of and distributions from the business.

The S Corporation Election

Eligible state-formed corporations and limited liability companies can elect to be treated as an S corporation for federal tax purposes by filing IRS Form 2553. This is not a separate state-formed entity, but a federal tax status designed to eliminate the double taxation inherent in a C corporation structure.

Key Features of the S Corporation Status:

Pass-Through Taxation: Business income and losses are passed through directly to the owners’ personal income tax returns, similar to the default classification of an LLC.

Potential Payroll Tax Savings: Owners who are employees of the entity can take a “reasonable salary” (subject to payroll tax) and receive any remaining profits as distributions (not subject to self-employment tax), which can offer significant tax savings.

To be eligible to make an S corporation election, the entity must meet and continue to comply with certain requirements, including:

Having no more than 100 shareholders or members.

Having only one class of stock.

Shareholders/members must be U.S. citizens or residents; certain trusts and estates are allowed, but partnerships, corporations, and non-resident aliens are generally not.

For a more in-depth discussion on tax classifications and available elections for business entities, please see our article, What should my business be classified as for tax purposes? .

Key Takeaways on Structure, Jurisdiction, and Tax:

Choose a Delaware Corporation: If you plan to seek venture capital, attract sophisticated investors, or operate across multiple states, despite the risk of double taxation.

Choose a Texas LLC: If your business is primarily Texas-focused, you prefer to avoid state personal and corporate income tax, and simplicity of compliance and a single level of federal income tax are a priority.

5. Step-by-Step Guide to Entity Formation

Once you have decided on your preferred structure and state of formation, the next step is the actual filing process. The discussion below addresses the steps to form a Delaware corporation and a Texas limited liability company. For a more in-depth discussion on documents to prepare when starting a business, including formation documents, please see our article, What documents should I prepare when starting my business? .

A. Forming a Delaware Corporation

The Delaware Division of Corporations handles all initial corporate filings.

Step 1: Verify Name and Availability

The name must be unique and contain a corporate identifier (e.g., “Corporation,” “Incorporated,” “Company,” “Limited,” or an abbreviation thereof). The use of certain words (e.g., “bank” or “university”) may require prior approval.

Use the Delaware Division of Corporations Name Availability Search Tool to confirm the availability of your desired name.

Step 2: Appoint a Registered Agent

Every Delaware entity must have a physical street address in Delaware and a registered agent to receive official legal and tax documents. If the principal place of business of the entity will not be in Delaware, the entity must appoint a registered agent that resides in the state. A registered agent can be an individual or a company.

A list of registered agents can be found on the Delaware Department of State’s website.

Step 3: File the Certificate of Incorporation

File the Certificate of Incorporation with the Delaware Division of Corporations.

This document must state the corporation’s name, the name and address of the registered agent, the name and address of the incorporator (the person or entity filing the Certificate), the nature of the business to be conducted, and the total number of authorized shares of stock and the par value of the shares in each class. The initial directors can be named in the Certificate of Incorporation or appointed by the incorporator when the initial organizational meeting is held.

Pay the applicable filing fee.

Step 4: Post-Formation Compliance

Draft and adopt corporate bylaws, the governing document for the corporation.

Hold an initial organizational meeting to approve the certificate of incorporation and bylaws, to appoint directors (if not named in the certificate of incorporation), to elect officers, and to issue stock.

Obtain a Federal Employer Identification Number (EIN) from the IRS.

File the Annual Report and pay any applicable franchise taxes (due March 1st following the year of incorporation).

B. Forming a Texas Limited Liability Company (LLC)

The Texas Secretary of State (SOS) handles all initial LLC filings.

Step 1: Verify Name and Availability

The name must be unique and contain an appropriate identifier (e.g., “Limited Liability Company,” “L.L.C.,” or “LLC”). The name cannot include words that imply illegal activities or affiliation with government agencies (e.g., “state department” or “university”). Names that suggest services requiring special licensing (e.g., “bank” or “attorney”) require prior authorization.

Use the Texas SOS’s SOSDirect online search portal to check existing business names.

Step 2: Appoint a Registered Agent

Every Texas entity must have a registered agent to receive official legal documents on behalf of the business. The registered agent can be an individual or a company (including the LLC itself) and must have a physical street address in Texas (not just a P.O. Box).

The registered agent must consent to the designation. An Acceptance of Appointment and Consent to Serve as Registered Agent (Form 401-A) can be used for this purpose. The consent must be retained by the LLC but does not need to be filed with the Texas SOS.

Step 3: File the Certificate of Formation

File the Certificate of Formation - Limited Liability Company (Form 205) with the Texas SOS.

This document must state the name of the LLC, the name and address of the registered agent, the name and address of the organizer, and the entity’s purpose.

Pay the applicable filing fee.

Step 4: Draft and Adopt an Operating Agreement

While not required to be filed with the state, a comprehensive Operating Agreement (or Company Agreement) is the most critical internal document. An Operating Agreement should address the governance and operations of the LLC, including ownership percentages, management structure, decision-making powers, and what happens when a member leaves.

Step 5: Post-Formation Compliance

Obtain a Federal Employer Identification Number (EIN) from the IRS.

File the annual Texas Franchise Tax Public Information Report (Form 05-102) and pay any applicable Texas Franchise Tax (due May 15th following the year of formation). The state waives the tax if revenue is below a certain threshold.

6. Moving Forward: Post-Formation Operations

Choosing the right legal entity is the critical first major step. After formation, there are several crucial ongoing compliance steps to maintain good standing and ensure legal operation.

Foreign Qualification (Doing Business in Other States)

When an entity operates outside of its state of formation (its “domestic” state), it is considered a “foreign” entity in those other states. If an entity transacts business in a foreign state, it is legally required to “qualify” or “register” that entity with the foreign state’s Secretary of State. What constitutes “transacting business” varies by state but common triggers include having a physical presence (e.g., office, warehouse), having employees, or regularly entering into contracts within that state.

Process: The entity files a Certificate of Authority (or similar document) in the foreign state, pays a fee, and designates a registered agent in that foreign state.

Consequence of Non-Compliance: Failure to qualify can result in fines, the inability to legally enforce contracts in that state’s courts, and back taxes.

Registering a DBA (Assumed Name)

If a business operates under a name different from its official, legal entity name, it must register that operating name as an “Assumed Name” or “Doing Business As” (DBA). This is typically filed at the county level, the state level, or both, depending on the jurisdiction.

Obtaining Permits and Licenses

Registration with the state is not a substitute for professional licensing or operational permits. Depending on your industry and location, a business may need:

Professional Licenses: Required for specific professions (e.g., accounting, law, medicine, contracting).

Local Permits: Zoning, building, health department, and fire department permits are often required by the city or county for operating a physical location.

Sales Tax Permits: Required by the state if you sell tangible goods or certain services.

Employer Tax Registration: If employees are anticipated, required at the federal level (and if applicable, the state level) before employees are paid. For a more in-depth discussion on obligations of an employer, please see our article, What are my obligations as an employer in Texas?.

Protecting Your Brand and Future

Trademark registration for national brand protection, intellectual property agreements, and confidentiality agreements are essential for safeguarding the company’s long-term assets.

Choosing the right structure is an investment in your business’s future stability and growth. While this guide provides a solid starting point, the nuances of multi-state operation, tax strategy, and investor relations require tailored legal advice.

Ready to start? Click here to schedule a consultation with Kalaria Law today and ensure your new venture is built on the strongest possible legal foundation.

Disclaimer: This article is for general informational purposes only and does not constitute formal legal advice.